前言

價值主張 (WHO you are? Business Aim?)

- Vision VISA願景是希望成為為任可人、在任可地點都可運作的支付網絡

- Mission 最安全、最可靠的全世界支付網絡

- 公司定位 全球支付科技公司

- 「中間人」: An intermediary between card issuers, its merchant partners, and its cardholders (Source: How does Visa make money?)

- 在解決現實面對的什麼問題? 可以讓不同銀行在支付領域上進行溝通 (資料來源: 【行行出狀元】支付 (Payment))

商業模型 (HOW do they run their business?)

- 業務核心邏輯 Issuer跟Acquirer是不同單位,所以需要VISA這一支付網絡作為溝通渠道 (包括交易資料傳遞及交易結算)來完成整個交易流程

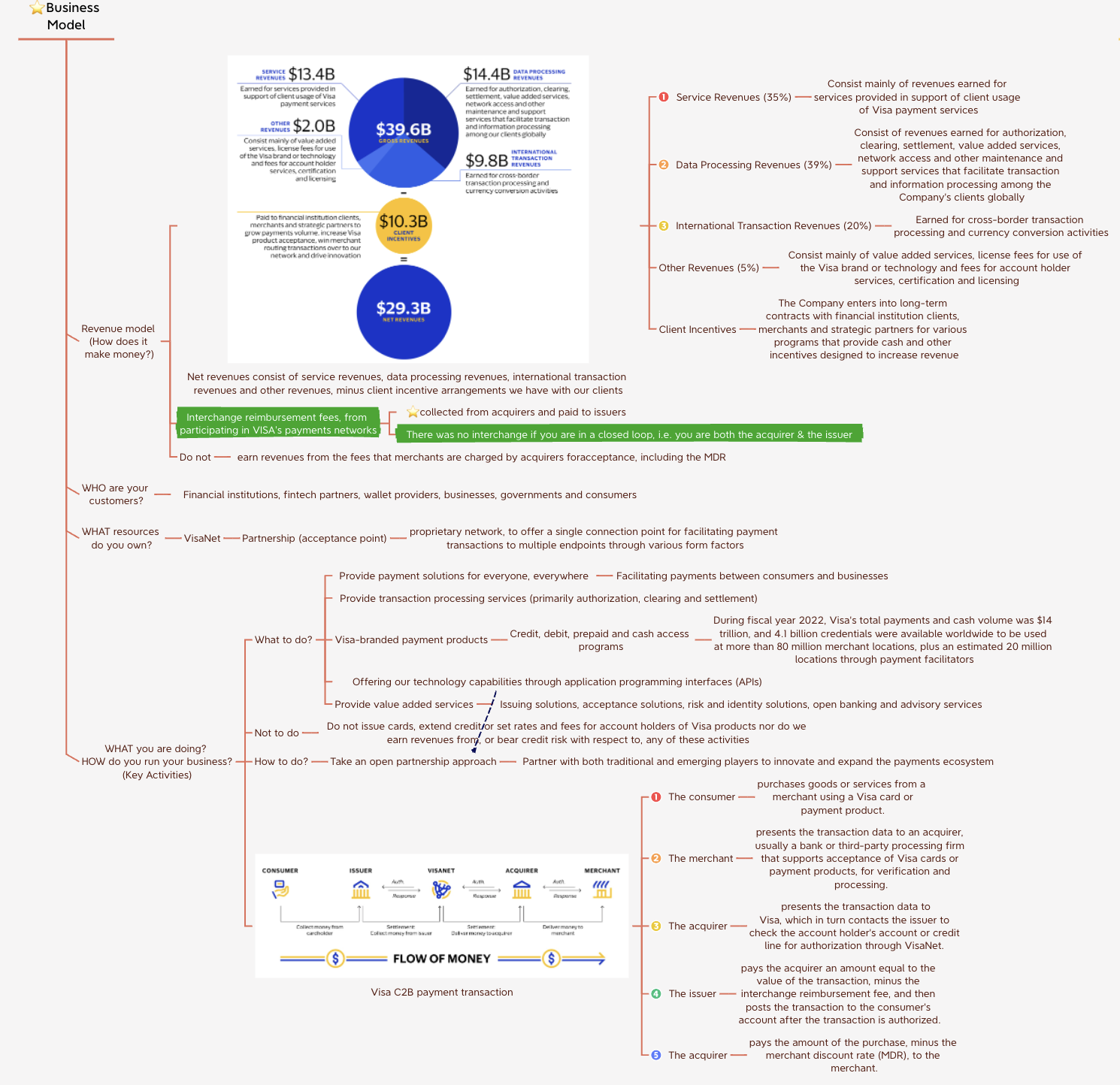

- 收入模型 (HOW do they charge their customers (earn their revenue)?)

- VISA收入是透過interchange fees (使用支付網絡後需要付出的費用,從銀行收取)反映 (Source: 全球支付研習社|外卡Interchange Fee費用全解析、How does Visa make money?)

- 收入包括服務收入(用戶使用VISA服務需要提供的費用,跟payment volume相關)、資料處理收入(交易結算、交收、網絡使用相關)、國際交易收入(跨境交易及換匯相關)及其他(Value-added services),而服務收入及資料處理收入佔公司超過70%收入

- 目標顧客 (Source: How does Visa make money?)

- Issuer (發卡行): VISA賦予發卡行發行信用卡的權力,同時向發卡行提供支付網絡,讓他們完成客戶交易

- Acquirer (收單行): 收單行向商戶提供VISA支付網絡連接入口

- 業務資源 VisaNet

- 營業活動

- 允許銀行發行Credit/Debit/Prepaid卡,從而讓持卡人使用VISA提供的支付網絡 (Source: How does Visa make money?)

產品/服務 (WHAT does it do?)

- 公司在賣什麼產品/服務給客戶來賺取收入?

- 消費支付: 重點就是我們日常作為顧客(To C)交易的應用,例如電子支付等

- 新流入

- "增量"是主要目的

- 主要流入貢獻為

- B2B

- 跨境交易及換匯

- VISA Direct: 全球即時轉帳網絡

- 附加服務

- "改善利潤率"是主要目的

業務增長點

- 原有增長點

- Covid後電子支付盛行

- 疫後通關的旅遊消費大增

- 電商需求繼續強大

- 第二曲線 (2nd curve)

- VISA Direct新流入繼續上升,而且用途慢慢擴大

- 附加服務新應用,例如open banking、cybersecurity等

- 支付創新科技公司及數碼銀行新合作

投資論點

- 買入理由 (投資邏輯)

- 跨境交易的地位無法被取代,因為已投入的基礎設施規模成為無所撼動的護城河

- 電子支付趨勢不可逆轉,電商等網上交易滲透率只會慢慢提高

- 由於資源豐富,早已開始佈局未來支付領域如Open Banking等。而且投資多家科技創投,或見到有潛力的公司或規模尚小的競爭對手會進行直接收購,如Tink、Currencycloud、Plaid等。

- 公司死亡理由

- 公司沒有定價權

- 主要的收入來源interchange fee cap會收激烈的同業競爭及政府監管所限制,例如

- 美國以外的interchange fee十分低,澳洲interchange fee cap低於20bps

- 支付網絡公司常因高昂的interchange fee被控告或排斥,例如英國Amazon跟VISA的衝突、Target控告Mastercard

- 未來高機會美國收緊interchange fee cap

- VISA支付網絡核心重點是Issuer跟Acquirer是不同單位,若果其中一個大型Acquirer具備發卡功能,那該銀行就可以直接跳過VISA完成整個交易流程 (e.g. Chase是美國最大的電商收單行,跟Amazon有支付上的合作)

- 中央銀行正研發國家級即時支付網絡,例如阿根廷、印度、巴西、加拿大及俄羅斯,均可取代VISA Direct的位置

指標

- 營運指標

- 年報有提及的

- Payment Volume

- Processed Transactions

- 其他重要metrics

- Credentials

- Cross-border volume

- 財務指標

- 年報有提及的

- Net Revenue

- Operating expense

- 其他重要metrics

- Free Cash Flow

Competitive Landscape

- Card Scheme

- Mastercard: Visa and Mastercard basically serve the same purpose, but there are some differences in acceptance, geographical revenue sources and the processing fees structure.

- American Express: Similarly as with Mastercard, the differences are, beyond the overall size, at a more narrow level, such as the processing fee structure.

- Non-card scheme

- Paypal: While Paypal is an online service that secures virtual payments using end-to-end encryption, Visa is a card network that facilitates transactions by connecting consumers, banks and merchants.

- Apple Pay: Apple Pay is a mobile payment and digital wallet service that allows users to make purchases with their Apple devices. In other words, Visa is the network that facilitates transactions, while Apple Pay is a specific service that utilizes Visa’s or other network to enable mobile payments.

- Google Pay. Same as Apple Pay. It’s a technology made to purchase things. It outsources payments processing to networks such as VisaNet.

Business Update

結語

- 產業擴張性及持續性: 支付行業的持續性是不容置疑的,充其量是支付方式的改變及行業「洗牌」。VISA作為支付網絡巨頭,在VAS上的投資也是巨大的,例如積極投入資源到歐洲Open Banking及security等安全領域上。

- 生活: 電子支付跟生活密不可分,特別是疫情後,無接觸支付、電商等使用需求大增。

- 反覆的需求: 信用卡基乎是每天都會使用的隨身物品,而且會重覆使用,所以行業穩定性高。

References

Appendix

- Content

- Products/Services (What VISA is doing?)

- Consumer Payment: Visa Token

- New Flows: Visa Direct

- Value-added services: Cybersource

- Value-added services: Tink

- ⭐️支付流程

- ⭐️商戶收款流程

- Earnings Transcript

1. Products/Services (What VISA is doing?)

Three growth levers: 1. Consumer payments

Three main pillars of our consumer payments enablement strategy: expanding access to credentials, increasing acceptance and deepening engagement

Three pillars of consumer payments: Expanding access to credentials

In FY22, the number of Visa credentials increased 9% year over year and were up 13%, excluding Russia.

We also crossed 4.8 billion tokens, security technology that protects sensitive data like credit card numbers, which helps Visa make payments both more secure and more convenient.

Visa now has more digital tokens than card credentials — and almost double last year. This marks a huge milestone both for the transition to digital and in our work to secure the wider payments ecosystem.

Three pillars of consumer payments: Increasing acceptance

In the face-to-face environment, consumer focus on safety and convenience is helping to drive preference for touchless commerce and tap to pay. Visa’s network also processed 70% more tap to ride transactions on global transit systems in FY22, surpassing one billion transactions for the first time ever.

Three pillars of consumer payments: Deepening engagement

Visa continues to make strategic investments in innovative technology and establish new partnerships and strengthen existing relationships. In the past fiscal year, we signed over 400 commercial partnerships with fintechs globally.

Security is also key to the future of digital money movement. Over the past five years, Visa has invested over $10 billion in technology, including to reduce fraud and enhance network security. In 2022 alone, Visa helped prevent an estimated $27 billion in fraud.

Three growth levers: 2. New Flows

Representing money movement beyond consumer to merchant payments — include business-to-business (B2B), business-to-consumer (B2C), government-to-consumer (G2C) and peer-to-peer (P2P) among others. (即是除了商戶跟消費者之間的交易)

The opportunity in B2B money movement continues to be enormous and our business in the space is significant, with nearly $1.5 trillion in payments volume this past year. Within B2B, our strategy is focused on card-based payments, cross-border payments and accounts receivable and payable payments.

In FY22, we continued to expand our client base geographically and in different segments, including fleet, healthcare and travel. For example, we signed a multi-year agreement with WEX to enable their travel, health and corporate clients to make payments using Visa’s virtual card capabilities.

Visa Direct

Use cases — like same-day payment for rideshare drivers, faster insurance payouts, remittances, early access to wages and real-time marketplace payouts — have shown ongoing appeal to consumers and businesses. For instance, eBay, one of the world’s largest third-party marketplaces, enabled faster payouts for its U.S. sellers via Visa Direct.

Through partnership, individuals and small businesses will be able to use Visa Direct to move money internationally to 78 digital wallet providers across 44 countries and territories. Partnership expands Visa Direct’s reach to nearly 7 billion endpoints, including more than 3 billion cards, over 2 billion accounts and 1.5 billion digital wallets.

Currencycloud

Visa also completed the acquisition of Currencycloud, a global platform that enables banks and fintechs to provide innovative foreign exchange solutions for cross-border payments, transact globally in multiple currencies, embrace digital wallet technology and embed financial tools into their businesses. Currencycloud continued to forge many new partnerships, having signed 135 since December 2021.

Three growth levers: 3. Value-added services

Visa’s value added services (VAS) enable both our traditional clients and new partners to deliver secure, reliable and convenient payments experiences for their customers. For Visa, where new flows means additional volume, VAS means additional yield on that volume.

Three strategies for continued growth: To deepen penetration of existing products

As a vital pillar of VAS, Cybersource (gateway solution for businesses to accept digital payments from all over the world) onboarded its one millionth merchant account earlier this year and continued to expand acquirer relationships, signing notable partnerships like Bank of New Zealand in FY22. In conjunction with Visa, Cybersource also powers dozens of transit projects in cities around the world, from multiple cities in Japan working in partnership with Sumitomo Mitsui Card Company, Limited, to Genoa’s Azienda Mobilità e Trasporti (AMT) in Italy.

Three strategies for continued growth: To grow our suite of value added products and solutions

In terms of new products and solutions, this year we completed our acquisition of Tink. Connected with more than 3,400 banks and financial institutions, Tink is an open banking platform that enables financial institutions, fintechs and merchants to move money and build financial products and services. These services give consumers more control over their financial experiences, from enabling account-to-account open banking powered payments to helping people manage their money and set financial goals. Just this year, Tink signed up marquee partners for open banking powered payments including the global payments platform Adyen and Revolut, the global financial super app with more than 20 million customers.

Three strategies for continued growth: To expand the geographical footprint of VAS

Across Europe, clients enrolling in Visa Advanced Authorization and Visa Risk Manager — two products that, together, give issuers both real-time risk scores to better inform authorization decisions and tools for managing risk — tripled over the past three years and these clients span 14 countries.

2. Consumer Payment: Visa Token

What is tokenization?

How Visa Token Service Works

How Tokens Are Used

3. New Flows: Visa Direct

What is it?

Aim

Who are the target users?

What can it do?

How is Visa Direct different from other solutions on the market?

Source: Q&A: What developers need to know about Visa Direct

4. Value-added services: Cybersource

What is it?

Aim

Who are the target users?

What can it do?

Source: Cybersource

5. Value-added services: Tink

What is it?

Aim

Who are the target users?

What can it do?

- Banking: Up the digital banking experience and increase operational efficiency with high-quality financial data. Open banking helps banks deliver sleek solutions to attract and engage customers while reducing risk.

- Lending: Tink connects lenders to consumers’ bank data to make real-time assessments based on consumers’ financial behaviour. More accurate data in risk assessments helps lenders accept more – at less risk.

- Payment: Tink brings together everything you need to create low-cost, high-performing payment journeys with open banking. Companies like Lydia and Kivra use Tink to manage payments, onboard customers, and more.

6. ⭐️支付流程

Authorization Flow

7. ⭐️商戶收款流程

Capture and Settlement Flow

8. Earnings Transcript

Key Highlights

- Consumer payment: Certainly excited about the realities of cash digitization. VISA is seeing in Tap to Pay, the fact that business in e-commerce has grown so much.

- New flows is driven by B2B recovery

- In new flows, VISA is putting a particular focus there on cross-border where previously a lot of the early use cases in new flows have been in the area of things like domestic, like P2P and B2B.

- Economic downturn may not affect much to company

- US Federal Reserve's enforcement of two unaffiliated networks to process every online US debit transaction beginning July 1 of 2023

- Resilient to high inflation: VISA is much more into everyday spend categories, e-commerce has evolved tremendously. There's been a lot more cash digitization. There still seems to be a lot of pent-up demand for travel and VAS are not necessarily all tied to economic ups and downs.

- Visa Direct

- Moat

- Use the VisaNet platform

- Acceptance: incredible reach with Visa Direct, almost 7 billion endpoints including accounts, cards and wallets

- You get a lot of the protections that you get, zero liability, chargebacks, dispute-good solid dispute management

- Use cases

- Cross-border remittances: you can do it account-to-account, account-to-account, account-to-account sitting at home. You don't have to go to someone to give them cash.

- P2P: a high volume but low yielding use case and very often it's the way VISA get going in most markets

Guidance

"Our planning assumptions get us to mid-teens constant dollar net revenue growth on a run rate basis, i.e., adjusted for Russia. With a 2-point Russia impact and a 4-point exchange rate headwind, reported nominal dollar fiscal year 2023 net revenue growth would be in the high single-digits."